Abdo and Kwong May Create Opportunities to File Protective Claims for Certain IRS Penalties and Interest

- Jun 23

- 4 min read

Updated: Jun 24

Two recent court decisions, Abdo v. Commissioner, 162 T.C. No. 7 (2024), and Kwong v. United States, 179 Fed. Cl. 38 (2025), may provide taxpayers with an opportunity to file protective claims relating to certain IRS penalties and interest connected to filing and payment deadlines affected by the COVID-19 federal disaster declaration. Taxpayers who paid failure-to-file penalties, failure-to-pay penalties, related interest, or certain other IRS penalties should consider reviewing their accounts promptly, given the potential July 10, 2026 protective filing deadline. Taxpayers with outstanding penalty assessments may also wish to consult their advisors regarding whether protective filings or other administrative remedies may be appropriate.

Why Abdo and Kwong Matter

In Abdo, the Tax Court held that the disaster relief provisions of Internal Revenue Code Section 7508A(d) require the postponement of certain tax deadlines during a federally declared disaster period. In Kwong, the U.S. Court of Federal Claims adopted a broader interpretation of those provisions, concluding that the COVID-19 federal disaster declaration effectively postponed many federal tax deadlines arising between January 20, 2020, and July 10, 2023. If the reasoning in Kwong ultimately prevails, some taxpayers may have grounds to challenge penalties and interest that accrued as a result of filing or payment obligations that arose during that period. Potentially affected items include failure-to-file penalties, failure-to-pay penalties, and related interest charges. These amounts may arise in connection with income, employment, estate, gift, and excise taxes, as well as certain international information return filing obligations. As a result, a broad range of taxpayers, including individuals, businesses, estates, and trusts, may wish to evaluate whether protective claims should be filed while the litigation remains unresolved.

What Is a Protective Claim?

Because the IRS does not currently agree with the broad interpretation adopted in Kwong, and the decision is being appealed, taxpayers generally should not expect automatic refunds or penalty abatements. However, they may be able to preserve their rights by filing a protective claim before the applicable statute of limitations expires. A protective claim allows the IRS to hold a taxpayer's claim open while the courts determine the ultimate outcome of the litigation. If a taxpayer waits until the litigation is resolved, it may be too late to seek relief.

Accordingly, taxpayers who have been assessed IRS penalties or interest should review their IRS account transcripts and related notices to determine whether they may have a viable claim.

How to File a Protective Claim Using IRS Form 843

Protective claims generally are paper filed on IRS Form 843, Claim for Refund and Request for Abatement. Taxpayers should clearly identify the submission at the top of the form as a "Protective Claim Pursuant to Kwong." The filing should include a statement describing the penalties, interest, and tax periods involved, together with copies of relevant IRS notices and account transcripts supporting the claim. Depending on the circumstances, a Form 843 may seek either a refund of penalties and interest that have already been paid, or abatement of penalties and interest that have been assessed but remain unpaid. Taxpayers should clearly describe the relief requested and explain why they believe the reasoning in Kwong supports the submitted claim.

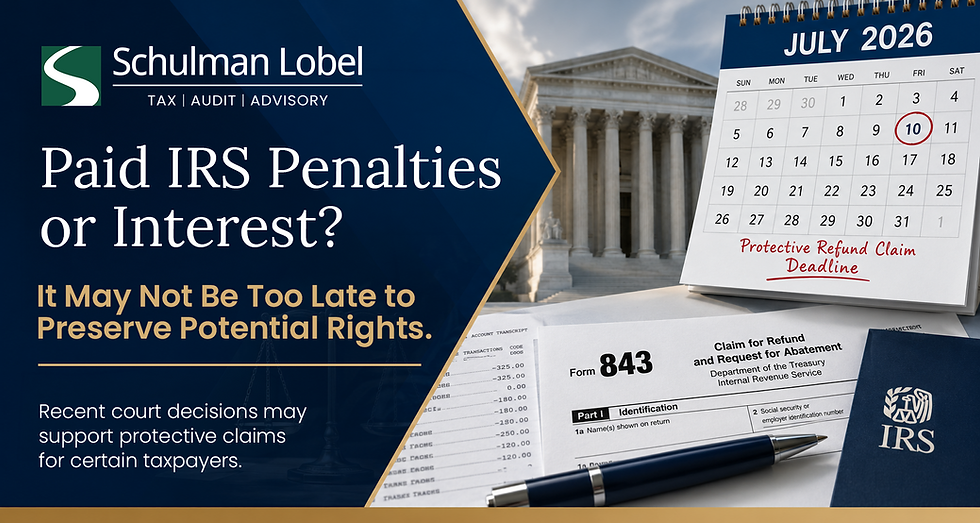

Why July 10, 2026 May Be an Important Date

In general, taxpayers may file a claim for credit or refund within the later of: (i) three years from the date the applicable return was filed, taking extensions into account, or (ii) two years from the date the tax, penalty, or interest was paid. Under the reasoning set forth in Kwong, the federally declared COVID-19 disaster period (from January 20, 2020, through July 10, 2023) may be disregarded in determining whether certain refund claims are timely. If that interpretation is ultimately sustained, some taxpayers may have substantially more time to file refund claims or protective claims than would otherwise be available under the normal limitation periods. The precise effect depends on each taxpayer's filing history, payment history, and the nature of the relief being requested. Different limitation periods may apply depending on whether the taxpayer is seeking a refund of amounts already paid or abatement of amounts that remain unpaid. In addition, the scope and continuing validity of Kwong remain the subject of ongoing litigation.

Accordingly, taxpayers who paid IRS penalties or interest should review their IRS account transcripts and related notices to determine whether they may have a viable claim. Many practitioners have identified July 10, 2026, as a conservative date by which protective claims should be filed to preserve potential rights while the courts continue to address the scope of Kwong. In some cases, the applicable limitations period may expire earlier, while in others it may extend beyond July 10, 2026, particularly where payments giving rise to the claim were made after July 10, 2023.

Take Action Before Potential Rights Expire

Taxpayers who paid IRS penalties or interest in connection with filing or payment obligations arising during the COVID-19 federal disaster period should consult with their Schulman Lobel advisor. Given the approaching deadline and the uncertainty surrounding the applicable limitation periods, taxpayers should evaluate potential claims promptly to avoid inadvertently losing the opportunity to seek a refund or other possible relief.

To discuss whether you may have a viable protective refund claim or to receive assistance preparing and submitting a claim, please contact Len Sprishen, J.D., LL.M., Partner, Schulman Lobel Advisors, LLC. Mr. Sprishen can help assess your specific circumstances, review applicable IRS records, and advise on steps that may be available to preserve your refund rights pending further developments in the litigation.

Comments